Proposed Rating Changes in England

Following the “Business Rates Review: Technical Consultation” , we report on the key future potential changes that the Government will introduce in England.

Ratepayer Self-Declaration

In a radical departure from the past and in an attempt to mirror other taxation, the Government is shifting the responsibility to ratepayers to keep the Valuation Office Agency (VOA) fully informed of any information that might impact their rating assessment.

Ratepayers will be expected to notify the VOA of any changes in relevant information, that is “information the VOA would need in order to identify the unit of property to be assessed…or assess its rateable value”.

This will include details about the ratepayer, the extent of the property they occupy and how it is used. Property factual information will include areas of different uses within a property, building specification and any other factors impacting its rating valuation.

C&W Comment – How realistic is it for ratepayers to know of all property changes that can impact their rating valuation?

Ratepayers will also need to notify the VOA of changes about any lease(s), licence(s) or other agreements concerning the use of the property. Meanwhile those ratepayers occupying properties requiring specialist rating valuations will have to provide details of their trade and accounts annually or any cost information on request.

Finally, all ratepayers will have to confirm annually that:

- They have provided details of any change in relevant information

- The data held by the VOA is correct

C&W Comment – This is a significant administrative and costly burden especially for ratepayers with large property portfolios. It is unlikely that ratepayers will hold data in the same way as the VOA e.g. a ratepayer might know the total sales and non-sales areas but not split according to the VOA valuation (zoned, masked area, lower quality area, etc.) so it will be extremely difficult for the ratepayer to confirm the accuracy of the VOA’s data. In addition, any ratepayer accruals for missed or incorrect assessments will potentially have to be declared.

How to Comply

A new online service will be provided for ratepayers. Ratepayers will need to access and sign up to the online service and follow the instructions, in the same way as other tax obligations. The Government’s view is that it is up to the ratepayer to find out what information they need to provide, although guidance will be provided on GOV.UK.

Once signed up, ratepayers will need to log into the online service to update their relevant information and complete their annual confirmation.

The Government proposes that ratepayers will have 30days to notify the VOA of any occupation, lease or property change. Those ratepayers who must submit details of their trade and accounts will have 30 days from 31 March. Similarly, ratepayers will only have 30 days to provide cost information following receipt of the request from the VOA.

C&W Comment – 30 days is too short a deadline for ratepayers to inform the VOA of every property change impacting their valuation e.g. installation of air conditioning, changing the use of a storage room to an office or staffroom, or lease change.

For the annual confirmation, ratepayers will need to confirm within 30 days of 31 March each year that they have met their obligations under the self-declaration duty during the previous year and that the data held by the VOA remains accurate and up to date.

C&W Comment – this period coincides with ratepayers dealing with new year rate demands and consequently should be moved to a quieter time of year e.g. June or September.

Although the Government do not plan to commence ratepayer self-declaration until the new online service is available, it will start during the 2023 Rating List.

Sanctions

The Government does not expect to introduce sanctions until 2026.

Penalties will be significant, but only become payable after a number of reminders. Failing to provide details of property changes impacting the assessment valuation will be based on 2% of the rateable value change, for lease changes up to £900 plus £60 per day until compliance and providing false information will be £500 plus 3% of the rateable value difference.

Ratepayers will also be prevented from appealing their assessment or having access to any VOA information on how their rateable values are calculated if they are not compliant with their duty of self-declaration including annual confirmation.

C&W Comment – the proposed sanctions are much higher than existing fines for not returning Forms of Return. Forgetting or overlooking property changes in particular could be onerous given penalties based on 2% of the rateable value linked to the property change.

Appeals Reform and Transparency

The Check stage of Check Challenge Appeal will be scrapped and a 3-month deadline for submitting compiled Challenges will be introduced from April 2026.

The Government claim that the deadline is required due to the shorter 3-yearly revaluation and to address concerns, draft assessments will be published several months prior to the new rating list.

C&W Comment – a 3-month deadline is unworkable. The deadline should be extended to 12 months after the publication of the draft rateable values (assuming this includes details of any evidence) to give ratepayers a realistic opportunity to satisfy themselves whether an appeal is required or not.

Appeals reform will coincide with the more significant phase 2 of greater transparency. The VOA will provide to ratepayers their full analysis of all rental evidence used to arrive at the rateable value for a property. However, the VOA will only provide the information after a request from the ratepayer.

C&W Comment – The VOA should be required to provide full evidence details when publishing draft rateable values rather than waiting for a ratepayer’s request. Given the short period to submit a compiled Challenge the VOA will be inundated with requests and will not be able to respond in time.

Phase 1 transparency to be implemented during the 2023 Rating List will be improved guidance covering rating principles and class-specific valuation approach.

Improvement Relief

A new 12-month improvement relief will be introduced in 2023 to support investment in property .

Ratepayers will need to meet two conditions - qualifying works and occupation.

Qualifying works must result in a rateable value increase. The relief is being targeted towards occupiers making improvements to support their business and consequently will exclude works where the property was not entered in a rating list during all or part of the works.

In order to meet the occupation condition ratepayers will have to satisfy the billing authorities that the property remained occupied by the same ratepayer during the period of the qualifying works.

The VOA will issue a certificate of the increase in rateable value so the billing authority can apply the 12-month relief.

C&W Comment – although welcome, we question how impactful 12 months rates relief will be on property improvement investment decisions.

Green Measures

Eligible plant and machinery used in onsite renewable energy generation and electricity storage, such as rooftop solar panels, wind turbines, and battery storage, plus electricity storage from any source where it is being used for electric vehicle charging points (EVCPs) will be exempt from business rates.

These measures were due in April 2023, but in his recent Spring Statement the Chancellor announced they will be brought forward 12 months to April 2022.

We will report the outcome of the above consultation in due course. Further Government consultations are expected with responses to the consultation “Online Sales Tax: Assessing an Option to Help Rebalance Taxation of the Retail Sector” required by 20 May and a consultation on transition following the 2023 Revaluation due later in 2022.

Rating Revaluation 2023 in Scotland

At each revaluation, the Assessor gathers rental evidence across all non-domestic properties. This information is used as the basis for establishing the Rateable Value of each property. All rental evidence is taken from a fixed date known as the 'Tone Date'. The 2023 Revaluation is based on rental evidence from 1 April 2022, which means that the Rateable Value will better reflect true market conditions.

It is imperative that ratepayers are adequately prepared for any changes to their Rateable Value that will take effect from 1 April 2023. These changes will form the basis of rates liabilities until at least 31 March 2026.

Our latest update sets out the proposed new rules that will govern the 2023 Revaluation Appeal Procedures, the implications for ratepayers, and how Cushman & Wakefield can assist in navigating the proposed changes.

Implications for Ratepayers

Cushman & Wakefield expect that each proprietor, tenant and occupier of a property will

retain the right to challenge the revised 2023 assessments irrespective of their actual liability. However, the current appeal system will be restructured to accommodate a new “two-stage” process. Initially, the appellant is required to outline the basis of their alternative proposal to the existing assessment, and then, in the absence of agreement, the proposal would be heard as an appeal before the Valuation Tribunal. The proposed two-Stage challenge process deviates from present appeal rules which simply allow for a letter of appeal to be lodged before 30 September in the year of a Revaluation.

The proposed procedural changes for challenging assessments represent a fundamental change to the existing procedures and appellants will be required to follow more complex appeal rules. The proposed changes place a greater onus on appellants to provide more detailed information in order to lodge a valid Stage 1 Proposal and removes the appellant’s right to introduce new evidence once the initial proposal is submitted.

Despite a more laborious appeal system, the time limit for lodging a "Proposal” is expected to reduce to 4 months, post revaluation (31 July 2023 deadline). This puts a significant burden on ratepayers to review the proposed assessments promptly once the draft figures are announced by the Assessor before the end of November 2022.

Even in times of valuation stability many revaluation assessments can be overstated by the Assessor.

The latest Scottish Government statistics show that the assessments of over 22,000 properties in Scotland were reduced after appeal. As such, it is our view that ratepayers must be able to review their proposed 2023 Rateable Value in a transparent manner because an inaccurate Rateable Value can lead to an excessive rates liability.

Circumstances leading up to the 2023 revaluation tone date have been anything but stable. The impact of Covid-19 and Brexit, amongst other significant global issues, have created volatility in many Scottish property markets in the lead up to the revaluation tone date. Market volatility means that valuation for rates purposes will be an even more difficult task for Assessors to complete accurately. Therefore appraising, reviewing and challenging the new 2023 Rateable Value will be of even greater importance for businesses.

Cushman & Wakefield strongly encourage clients to consider the implications of the 2023 Revaluation as soon as possible. Clients should ascertain whether there is a possibility for Pre-Agreeing their Rateable Value with your local Assessor prior to the 2023 Revaluation coming into force.

The clear benefit of Pre-Agreement is that it negates the need to utilise what could be a lengthy, uncertain, and onerous new appeal system and provide clear visibility of rating liabilities from day one of the Revaluation.

Material Change of Circumstance Appeals (MCC)

The Scottish Government is in the process of introducing legislation that will effectively "invalidate" all Material Change of Circumstances (MCC) valuation appeals lodged by ratepayers as a response to the impact of the Covid-19 pandemic. To this end, the Scottish Government introduced draft legislation, the Non Domestic Rates (Coronavirus) (Scotland) Bill, into the Scottish Parliament earlier this year.We anticipate this Bill will shortly be passed by the Parliament and consequently, the many thousands of Covid-19 MCC appeals that were lodged on behalf of our clients will not provide any further rate savings.

Penalties for non-compliance with return of information requests

The Scottish Government has also increased the scale of penalties for non-return of Local Authority Information Notices. Specifically, the new provisions entitle the Assessor to request information relating to rental levels, turnover details and construction costs. Requests can be sent to any person that the Assessor thinks is a proprietor, tenant or occupier of lands and heritages that are to be valued or any other person who the Assessor thinks has information. These provisions provide the Assessor with significantly greater information gathering powers and we anticipate that there will be a large increase in requests for information.Failure to provide the requested information to the Assessor may lead to a substantial fine, calculated as follows:

| Stage 1 | Stage 2 | Stage 3 | |

|---|---|---|---|

| Period from date when the Information notice is issued | 28 Days | 70 Days | 84 Days |

| Penalty for non-return if lands and heritages are entered within the Valuation Roll | £200 or 1% of RV (whichever greater) | £1,000 or 20% of RV (whichever greater) | £1,000 or 50% of RV (whichever greater) |

| Penalty if lands and heritages not entered within Valuation Roll | £1,000 | £10,000 | £50,000 |

| Stage 1 | 28 Days | £200 or 1% of RV (whichever greater) | £1,000 |

| Stage 2 | 70 Days | £1,000 or 20% of RV (whichever greater) | £10,000 |

| Stage 3 | 84 Days | £1,000 or 50% of RV (whichever greater) | £50,000 |

Cushman and Wakefield have worked closely with the Scottish Assessors Association to facilitate a “bulk-return” of information across entire portfolios, which avoids the need for the Assessor to issue singular requests. This type of return reduces the risk of an unnecessary penalty where the information is not returned to the Assessor in respect of a singular property and may appeal to clients that have multiple properties large portfolios.

We would welcome discussing these, or any other items and potential implications of the forthcoming 2023 Rates Revaluation with you further.

Non-Domestic Rates (Business Rates) in Wales

The Welsh Rating List is very similar to the English List, in how the valuation is arrived at. All properties in the Rating List are valued at a set date with certain assumptions to arrive at the Rateable Value (the set date and majority of assumptions are consistent with England). Currently the Rating List dates are aligned with England with the 2017 List coming to an end on 31/3/2023 and the next three yearly list commencing on 1/4/2023.

Since devolution, Wales has not always followed England’s approach to rating legislation, with regards to how appeals are dealt with and various rate reliefs. We have listed below three of the main differences from England.

1. Appeals/ CCA

Wales chose not to align their appeals system with the English system from 2010. Wales did not introduce the requirement to serve a statement of case ahead of Tribunal hearings in 2010 and they do not have the Check Challenge Appeal system that England in 2017. The current approach in Wales is as follows:

- An appeal is submitted to the Valuation Office Agency (VOA). No reasons for appeal or evidence are required at this stage.

- The appeal is programmed for a two-month discussion period with the VOA between 3-12months later. Evidence is requested at this point and discussion should be completed.

- If not resolved during the discussion period, then the appeal is forwarded to Valuation Tribunal for a hearing.

We aim to disclose all our evidence to VOA at the earliest opportunity, but it is not unusual for the case to be listed for a hearing without a discussion taking place and VOA often requesting a postponement of the hearing to investigate or even inspect the property.

There have been suggestions that Wales may move in line with England’s approach for future lists. Currently there are no details of whether Wales will continue with this system for the 2023 Revaluation. It is likely the Welsh Government is observing how the proposed legislative changes in England work before deciding what should be adopted in Wales..

2. Transition and Other Reliefs

Welsh parliament chose not to have a Ttransition Scheme in 2017. With the majority of rating assessments reducing in value between 2010 and 2017 Rating Lists and only a few properties staying the same or increasing, this has been a big positive to ratepayers in Wales seeing the benefit of the assessment reductions in their payments.

When England introduced additional relief because of Covid-19, Wales also introduced similar reliefs, but with slightly different criteria and lists of applicable properties.

3. Splitting of Non-Domestic Properties in Wales for Valuation Purposes

In 2015 the Supreme Court ruled, in the case of Woolway (VO) v Mazars. The ruling of the Court meant that individual floors were often treated as separate hereditament (rating unit) irrespective of whether the hereditaments werein the same occupation and contiguous. As a result, some ratepayers who were previously receiving only one rates bill started toreceive two or more. In most cases, liability also increased with the loss of quantum discount.

In 2018 the UK Government passed legislation to reinstate the VOA’s previous practice with respect to rating in England. This gave all ratepayers the opportunity to appeal their assessments, merge hereditaments that were previously a single assessment and backdate any amendment to the values prior to the Supreme Court ruling.

The Welsh government did not follow the English lead in 2018 although they have been lobbied to do so. Finally, in March 2022 the Welsh Government commenced a consultation to amend the legislation but only effective from 2023.

We will make strong arguments that the changes should be backdated to make sure ratepayers are not penalised compared to their English counterparts.

Extended Rate Reliefs 2022/23

England

The 2022/23 Retail, Hospitality and Leisure Business Rates Relief scheme will provide eligible, occupied, retail, hospitality and leisure properties with a 50% relief, up to a cash cap limit of £110,000 per business.

How much relief will be available?

Subject to the £110,000 cash cap per business, the total amount of government-funded relief available for each property for 2022/23 under this scheme is:

- For chargeable days from 1 April 2022 to 31 March 2023, 50% of the chargeable amount.

- Ratepayers that occupy more than one property will be entitled to relief for each of their eligible properties up to the maximum £110,000 cash cap, per business.

Government cash caps and subsidy control

From 1 April 2022, relief will be capped at £110,000 per business. Under the cash cap, no ratepayer can in any circumstances exceed the £110,000 cash cap across all of their hereditaments in England.

This relief falls within the Small Amounts of Financial Assistance Allowance allowing up to £343,000 in a three-year period (consisting of the 2022/23 year and the two previous financial years). Expanded Retail Discount granted in either 2020/21 or 2021/22 does not count towards the £343,000 allowance, but BEIS business grants (throughout the 3 years) and any other subsidies claimed under the Small Amounts of Financial Assistance limit should be counted.

Wales

Retail, leisure and hospitality ratepayers in Wales will receive 50% non-domestic rates relief for the duration of 2022-23. Like the scheme announced by the Government, the Welsh Government’s Retail, Leisure and Hospitality Rates Relief scheme will be capped at £110,000 per business across Wales.

Government cash caps and subsidy control

The scheme is considered by the Welsh Government to be outside the scope of any international trade agreements as measures are focused locally within Wales. Consequently, this does not fall within the £343,000 subsidy control allowance.

Scotland

The Scottish Government has extended Retail, hospitality and leisure relief for 3 months until 30 June 2022 and for these 3 months eligible ratepayers are entitled to 50% relief up to a maximum of £27,500 per business.

COVID-19 Additional Relief Fund (CARF)

The Government has announced a new COVID-19 Additional Relief Fund (CARF) of £1.5 billion which has been distributed to Local Authorities to administer a discretionary relief for Business Rates.

The aim of this scheme is to provide Business Rates relief for the financial year 2021/2022 to businesses who have been adversely affected by the pandemic and are ineligible for existing support linked to business rates. With any credits carried forward to reduce liability for 2022/23.

Basic principles

It is for local authorities to determine the criteria and the level of relief for individual hereditaments. However, the Government has set basic principles for the scheme which must be followed:

- it can only be awarded in respect of business rate liability for 2021/2022

- it cannot be awarded for periods where the premises are classed as empty

- it cannot be applied to business premises already in receipt of, or potentially entitled to Extended Retail Discount

- it cannot be awarded where 100% in total relief is already being claimed. For example, businesses in receipt of 100% small business rates relief will not be eligible

- it cannot be awarded to public sector organisations

- it cannot be awarded to businesses that are beneficiaries of public funds equal to, or in excess of subsidy limits within the UK-EU Trade and Cooperation Agreement (TCA) or will exceed those limits if a CARF relief is awarded.

The CARF scheme is subject to the subsidies chapter within the UK-EU Trade and Cooperation Agreement (TCA).

Subsidy allowance

There are 3 possible subsidy allowances:

- Small Amounts of Financial Assistance Allowance – limit of £335,000 (subject to exchange rates) in Small Amounts of Financial Assistance over any rolling period of 3 financial years

- COVID-19 Business Grant Allowance – limit of £1,900,000 across all COVID-19 Business Grant schemes

- COVID-19 Business Grant Special Allowance - if limits under the Small Amounts of Financial Assistance Allowance and COVID-19 Business Grant Allowance have been reached, it may be possible access a further allowance of funding under these scheme rules of up to £10,000,000 across all COVID-19 Business Grant schemes

Grants under these 3 allowances can be combined for a potential total allowance of up to £12,235,000 (subject to exchange rates).

Impact of the 2023 Revaluation

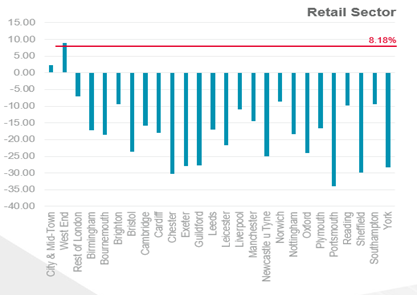

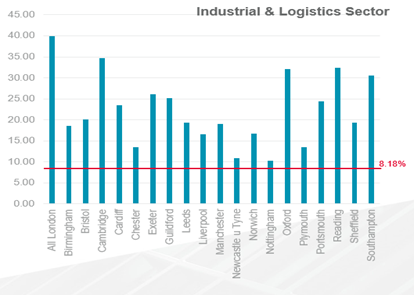

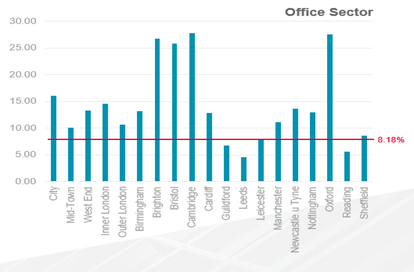

Early research by Cushman & Wakefield into the impact of the forthcoming 2023 Revaluations suggests the revaluations will be one of the most redistributive ever. The revaluations will cause a significant shift of rates liability from retail to the logistics sector. Meanwhile the office sector will see a more modest increase.

2023 Revaluations are planned for all the home countries but with differing valuation dates. In England and Wales the new 2023 Rateable values will be based on rental values as at 1 April 2021, in Northern Ireland 1 October 2021 and Scotland 1 April 2022.

In England, Wales and Scotland the existing 2017 Rateable Values are all based on April 2015 rental levels. The change in rateable values therefore will mirror rental value change between April 2015 and 2021 (or 2022 for Scotland).

Revaluations are revenue neutral in real terms, with multipliers applied to assessments to calculate liability adjusted according to aggregate rateable value movement. For example, if total rateable value increases by 5%, the multiplier will be reduced by the same percentage before being adjusted for inflation.

Consequently, it is a property’s rateable value change compared to the average which determines whether a liability increases or falls following a revaluation.

Research Findings

Our research sought to compare expected rateable value movements by sector and in key locations. Using mean figures by sector and/or location hides wide percentage variations at property level. Nevertheless, our research does reveal likely trends of rates liability change.

Our research suggests that within England and Wales rateable values overall will increase by 8.18%. It was too early to calculate overall rateable value change in Scotland given the later valuation date. However, early indications suggest very little change overall in Scotland.

Meanwhile the average change by sector in England and Wales will be:

- Retail -8.7% (-19.5% excluding London)

- Industrial & Logistics +31.0%

- Offices +13.8%

Retail sector rates liability will fall on average 13% (23% excluding London) whereas the Industrial & Logistics Sector will see an average 25% increase. The Office sector will also experience an average increase of 10% in rates liability.

In Scotland, the same sector redistributions are repeated albeit to a lesser extent.

Turning to key locations in each sector, wherever the average expected rateable value percentage change is higher than the overall 8.18% average, rates liability will increase from 2023/24.

Our research suggests retail liability in all our key locations, with the exception of London’s West End, will fall. Meanwhile industrial & logistics sector will see liability increases in all key locations with

London, Cambridge, Oxford, Reading and Southampton experiencing the highest average liability increases of over 25%.

Within the office sector, the highest average liability increases will be in Brighton, Bristol, Cambridge and Oxford. Meanwhile office liabilities will fall overall in Guildford, Leeds and Reading.

Transition

Transition is largely limited to England and could have a significant impact on rates liability following the 2023 Revaluation.

Transition effectively “phases” any large liability change - whether an increase or fall. Downwards “phasing” in particular is seen as being unfair to ratepayers whose assessments have fallen in line with rental values but are left with artificially high rate liabilities for years.

Retailers in particular will be keen to ensure that transition does not impact their expected fall of liabilities after the 2023 Revaluation. Meanwhile, ratepayers within the Industrial & Logistics Sector will hope that transition affords them some protection from a sudden high increase of liability in 2023/24.

Given the 2023 Rating List will only last three years, previous transition schemes will not work. The Government is due to consult later this year on whether there should be any transition for the 2023 Revaluation and what form any transition might take.

MEET THE TEAM

RELATED SERVICES

Business Rates

Vacating An Existing Property

Various measures exist that allow occupiers and landlords to minimise their business rates liability prior to a lease break or after a termination date.

Lease Transaction & Advisory

Cushman & Wakefield is one of the world’s leading providers of leasing advice to occupiers and investors.

More Insights

Article • Sustainability / ESG

Landlords vs Tenants: Future MEES Conflicts

Research

MarketBeat

UK Elderly Care MarketBeat Reports